Tax-smart investing

Taxes can have a significant impact on your investment returns. We seek to apply a range of different tax-smart investing strategies designed to help you keep more of what you earn, so your money stays invested and working for you.

Unlike some firms that simply wait until year end to harvest tax losses, we take an ongoing, tax-efficient approach that seeks to enhance after-tax returns—when we establish your portfolio, in our day-to-day management of your investments, and when you need to withdraw money.

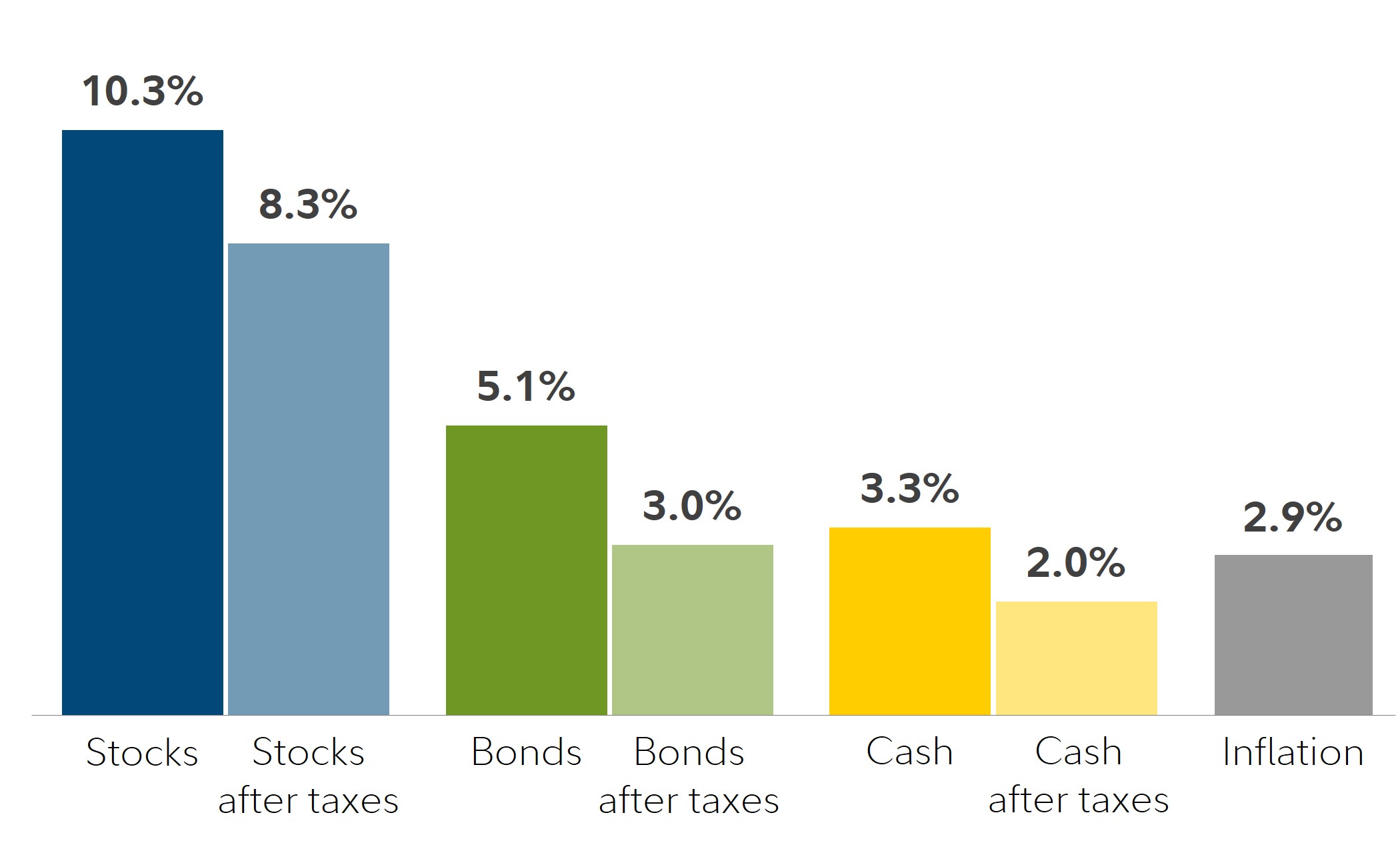

Taxes Can Significantly Reduce Returns2

AVERAGE ANNUAL RETURN PERCENTAGE

HISTORIC MARKET PERFORMANCE: 1926—2023

FOR ILLUSTRATIVE PURPOSES ONLY.

More information

1. Tax-smart (i.e., tax-sensitive) investing strategies (including tax-loss harvesting) are applied in managing certain taxable accounts on a limited basis, at the discretion of the portfolio manager primarily with respect to determining when assets in a client's account should be bought or sold. As the discretionary portfolio manager, Strategic Advisers LLC ("Strategic Advisers") may elect to sell assets in an account at any time. A client may have a gain or loss when assets are sold. There are no guarantees as to the effectiveness of the tax-smart investing strategies applied in serving to reduce or minimize a client's overall tax liabilities, or as to the tax results that may be generated by a given transaction. Strategic Advisers does not currently invest in tax-deferred products, such as variable insurance products, or in tax-managed funds, but may do so in the future if it deems such to be appropriate for a client. Strategic Advisers does not actively manage for alternative minimum taxes; state or local taxes; foreign taxes on non-U.S. investments; federal tax rules applicable to entities; or estate, gift, or generation-skipping transfer taxes. Strategic Advisers relies on information provided by clients in an effort to provide tax-sensitive investment management and does not offer tax advice. Except where Fidelity Personal Trust Company (FPTC) is serving as trustee, clients are responsible for all tax liabilities arising from transactions in their accounts, for the adequacy and accuracy of any positions taken on tax returns, for the actual filing of tax returns, and for the remittance of tax payments to taxing authorities.

2. Taxes Can Significantly Reduce Returns data, Morningstar 2024 and Precision Information, dba Financial Fitness Group 2023 12/31/2023. All rights reserved. Past performance is no guarantee of future results. This chart is for illustrative purposes only and does not represent actual or future performance of any investment option. Stocks after taxes assumes that the stocks purchased were held for five years, then sold, and the capital gains realized. The net proceeds from the sale were invested. Dividends were taxed when earned and reinvested. Bonds were turned over 28 times within the 96-year period. Capital gains were realized at the time of sale and reinvested. Government bonds and Treasury bills are guaranteed by the full faith and credit of the United States government as to the timely payment of principal and interest, while stocks are not guaranteed and have been more volatile than other asset classes.

Market indexes are included for informational purposes and for context with respect to market conditions. All indexes are unmanaged, and performance of the indexes includes reinvestment of dividends and interest income, unless otherwise noted. Securities indices are not subject to fees and expenses typically associated with managed accounts or investment funds. Review the definitions of indexes for more information. Please note an investor cannot invest directly into an index.

Federal income tax is calculated using historical marginal and capital gains tax rates for a single taxpayer earning $120,000 in 2015 dollars every year. This annual income is adjusted using the Consumer Price Index in order to obtain the corresponding income level for each year. Income is taxed at the appropriate federal income tax rate as it occurs. When realized, capital gains are calculated assuming the appropriate capital gains rates. The holding period for capital gains tax calculation is assumed to be five years for stocks, while government bonds are held until replaced in the index. No state income taxes are included.

Stocks are represented by the Ibbotson® Large Company Stock Index. Government bonds represented by the 20-year U.S. government bond, cash by the 30-day U.S. Treasury bill, and inflation by the Consumer Price Index. An investment cannot be made directly in an index. The data assumes reinvestment of income and does not account for transaction costs.

Keep in mind that investing involves risk. The value of your investment will fluctuate over time, and you may gain or lose money.

Diversification and asset allocation do not ensure a profit or guarantee against loss.

Generally, among asset classes stocks are more volatile than bonds or short-term instruments and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Although the bond market is also volatile, lower-quality debt securities including leveraged loans generally offer higher yields compared to investment grade securities, but also involve greater risk of default or price changes. Foreign markets can be more volatile than U.S. markets due to increased risks of adverse issuer, political, market or economic developments, all of which are magnified in emerging markets.

Fidelity does not provide legal or tax advice. The information herein is general and educational in nature and should not be considered legal or tax advice. Tax laws and regulations are complex and subject to change, which can materially impact investment results. Fidelity cannot guarantee that the information herein is accurate, complete, or timely. Fidelity makes no warranties with regard to such information or results obtained by its use, and disclaims any liability arising out of your use of, or any tax position taken in reliance on, such information. Consult an attorney or tax professional regarding your specific situation.

Other than with respect to assets managed on a discretionary basis through an advisory agreement with Strategic Advisers LLC, you are responsible for determining whether, and how, to implement any financial planning recommendations presented, including asset allocation suggestions, and for paying applicable fees. Financial planning does not constitute an offer to sell, a solicitation of any offer to buy, or a recommendation of any security by Fidelity Investments or any third party.

Fidelity® Wealth Services provides non-discretionary financial planning and discretionary investment management through one or more Personalized Portfolios accounts for a fee. Advisory services offered by Strategic Advisers LLC (Strategic Advisers), a registered investment adviser. Brokerage services provided by Fidelity Brokerage Services LLC (FBS), and custodial and related services provided by National Financial Services LLC (NFS), each a member NYSE and SIPC. Strategic Advisers, FBS, and NFS are Fidelity Investments companies.

Fidelity Brokerage Services LLC, Member NYSE, SIPC, 900 Salem Street, Smithfield, RI 02917

Asset location

For qualifying goals, we may strategically position assets across your Personalized Portfolios accounts based on their tax registration to help enhance your after-tax returns. Asset location may also increase the impact of some of our other tax management strategies.

Harvest tax losses2

If we sell positions in your account at a loss, those losses can be used to offset gains in your Personalized Portfolios accounts or elsewhere in your portfolio, which can help reduce your tax liability in either the current year or in future years.

Invest in municipal bond funds or ETFs

When it makes sense based on your tax rate, we may seek to provide exposure to municipal bonds, whose interest may be exempt from federal taxes. Depending on your state of residence, interest may also be exempt from state and local taxes.

Manage capital gains

When possible, we may realize long-term capital gains instead of short-term gains, which may reduce your tax obligations.

Manage exposure to distributions

We'll seek investments that pay out fewer or no distributions to help reduce your tax obligations.

Tax-smart rebalancing

As markets move and your mix of investments shifts, we'll consider the potential tax impact of trades we make on your behalf when maintaining the appropriate level of risk.

Transition management

We search for ways to integrate your existing eligible holdings3 into your managed account as opposed to selling all of your existing investments in order to "start from scratch." This can help reduce the potential tax consequences of creating your personalized investment strategy.4

Tax-smart withdrawals

When you need to withdraw money, we'll seek to reduce the tax impact of those withdrawals when selecting which holdings to sell.

More information

1. Tax-smart (i.e., tax-sensitive) investing strategies (including tax-loss harvesting) are applied in managing certain taxable accounts on a limited basis, at the discretion of the portfolio manager primarily with respect to determining when assets in a client's account should be bought or sold. As the discretionary portfolio manager, Strategic Advisers LLC ("Strategic Advisers") may elect to sell assets in an account at any time. A client may have a gain or loss when assets are sold. There are no guarantees as to the effectiveness of the tax-smart investing strategies applied in serving to reduce or minimize a client's overall tax liabilities, or as to the tax results that may be generated by a given transaction. Strategic Advisers does not currently invest in tax-deferred products, such as variable insurance products, or in tax-managed funds, but may do so in the future if it deems such to be appropriate for a client. Strategic Advisers does not actively manage for alternative minimum taxes; state or local taxes; foreign taxes on non-U.S. investments; federal tax rules applicable to entities; or estate, gift, or generation-skipping transfer taxes. Strategic Advisers relies on information provided by clients in an effort to provide tax-sensitive investment management and does not offer tax advice. Except where Fidelity Personal Trust Company (FPTC) is serving as trustee, clients are responsible for all tax liabilities arising from transactions in their accounts, for the adequacy and accuracy of any positions taken on tax returns, for the actual filing of tax returns, and for the remittance of tax payments to taxing authorities.

2. Tax-smart investing strategies, including tax-loss harvesting, are applied in managing certain taxable accounts on a limited basis, at the discretion of the portfolio manager, Strategic Advisers LLC (Strategic Advisers), primarily with respect to determining when assets in a client's account should be bought or sold. Assets contributed may be sold for a taxable gain or loss at any time. There are no guarantees as to the effectiveness of the tax-smart investing strategies applied in serving to reduce or minimize a client's overall tax liabilities, or as to the tax results that may be generated by a given transaction.

3. For a list of eligible investments, contact a Fidelity representative. Clients may elect to transfer noneligible securities into their accounts. Should they do so, Strategic Advisers or its designee will liquidate those securities as soon as reasonably practicable, and clients acknowledge that transferring such securities into their accounts acts as a direction to Strategic Advisers to sell any such securities. Clients may realize a taxable gain or loss when these shares are sold, which may affect the after-tax performance/return within their accounts, and Strategic Advisers does not consider the potential tax consequences of these sales when following a client's deemed direction to see such securities. Strategic Advisers reserves the right not to accept otherwise eligible securities, at its sole discretion.

4. While Strategic Advisers does consider the potential tax consequences of the sale of eligible securities used to fund an account managed with tax-smart investing strategies, Strategic Advisers believes that appropriate asset allocation and diversification are of primary importance and applies tax-smart investing strategies as a secondary consideration in managing such accounts. Accordingly, clients who fund an account managed with tax-smart investing strategies with appreciated securities should understand that Strategic Advisers could sell such securities notwithstanding that the sale could trigger significant tax consequences.

Keep in mind that investing involves risk. The value of your investment will fluctuate over time, and you may gain or lose money.

Diversification and asset allocation do not ensure a profit or guarantee against loss.

Generally, among asset classes stocks are more volatile than bonds or short-term instruments and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Although the bond market is also volatile, lower-quality debt securities including leveraged loans generally offer higher yields compared to investment grade securities, but also involve greater risk of default or price changes. Foreign markets can be more volatile than U.S. markets due to increased risks of adverse issuer, political, market or economic developments, all of which are magnified in emerging markets.

Fidelity does not provide legal or tax advice. The information herein is general and educational in nature and should not be considered legal or tax advice. Tax laws and regulations are complex and subject to change, which can materially impact investment results. Fidelity cannot guarantee that the information herein is accurate, complete, or timely. Fidelity makes no warranties with regard to such information or results obtained by its use, and disclaims any liability arising out of your use of, or any tax position taken in reliance on, such information. Consult an attorney or tax professional regarding your specific situation.

Other than with respect to assets managed on a discretionary basis through an advisory agreement with Strategic Advisers LLC, you are responsible for determining whether, and how, to implement any financial planning recommendations presented, including asset allocation suggestions, and for paying applicable fees. Financial planning does not constitute an offer to sell, a solicitation of any offer to buy, or a recommendation of any security by Fidelity Investments or any third party.

Fidelity® Wealth Services provides non-discretionary financial planning and discretionary investment management through one or more Personalized Portfolios accounts for a fee. Advisory services offered by Strategic Advisers LLC (Strategic Advisers), a registered investment adviser. Brokerage services provided by Fidelity Brokerage Services LLC (FBS), and custodial and related services provided by National Financial Services LLC (NFS), each a member NYSE and SIPC. Strategic Advisers, FBS, and NFS are Fidelity Investments companies.

Fidelity Brokerage Services LLC, Member NYSE, SIPC, 900 Salem Street, Smithfield, RI 02917