Tax-smart investment1A comprehensive suite of strategies designed to help you reach your goals faster. |

Transition management

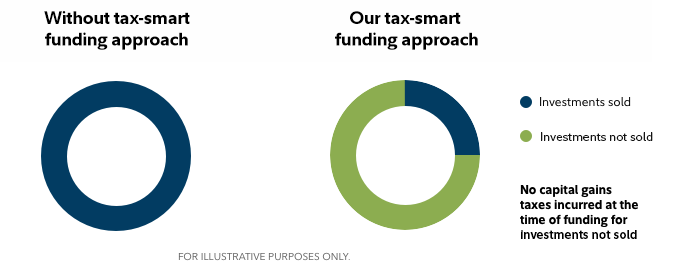

When building your strategy, we take a personalized approach, carefully considering which investments to keep and which to sell. Our goal is to reach your desired asset allocation while reducing potential capital gains taxes. If you have holdings that we believe fit within your investment strategy, we'll look to integrate them into one or more of your Personalized Portfolios accounts2 as opposed to selling all your existing investments in order to "start from scratch." This can help reduce the potential tax consequences of building your investment strategy. Note that the use of asset location can enhance the effectiveness of this strategy.

Tax-smart withdrawals

When clients need to withdraw money from their accounts, those withdrawals generally involve selling securities, which usually results in taxes. However, with careful planning, there are things that can be done that may help reduce those taxes. This approach is called tax-smart withdrawals and depending on the tax registration of the accounts we're managing on your behalf, it can take many forms.

For instance, if we know a client will need to take periodic withdrawals, like required minimum distributions (RMDs), the investment team can maintain cash positions in order to facilitate those withdrawals. If an account's cash holdings fall below a certain threshold and securities need to be sold, we can look at individual tax lots for investments that have appreciated less, or that have been held for longer than one year—two factors that can reduce the tax impact of those sales.

In cases where we're managing accounts with different tax registrations, we may choose to sell assets from some accounts and not others in an effort to reduce the tax impact. More importantly, we can do this while still maintaining the appropriate goal asset allocation in an effort to ensure that clients' investments remain aligned with their goals.

1. Tax-smart (i.e., tax-sensitive) investing techniques (including tax-loss harvesting) are applied in managing certain taxable accounts on a limited basis, at the discretion of the portfolio manager primarily with respect to determining when assets in a client's account should be bought or sold. As the discretionary portfolio manager, Strategic Advisers LLC ("Strategic Advisers") may elect to sell assets in an account at any time. A client may have a gain or loss when assets are sold. There are no guarantees as to the effectiveness of the tax-smart investing techniques applied in serving to reduce or minimize a client's overall tax liabilities, or as to the tax results that may be generated by a given transaction. Strategic Advisers does not currently invest in tax-deferred products, such as variable insurance products, or in tax-managed funds, but may do so in the future if it deems such to be appropriate for a client. Strategic Advisers does not actively manage for alternative minimum taxes; state or local taxes; foreign taxes on non-U.S. investments; federal tax rules applicable to entities; or estate, gift, or generation-skipping transfer taxes. Strategic Advisers relies on information provided by clients in an effort to provide tax-sensitive investment management and does not offer tax advice. Except where Fidelity Personal Trust Company (FPTC) is serving as trustee, clients are responsible for all tax liabilities arising from transactions in their accounts, for the adequacy and accuracy of any positions taken on tax returns, for the actual filing of tax returns, and for the remittance of tax payments to taxing authorities.

2. For a list of eligible investments, contact a Fidelity representative. Clients may elect to transfer noneligible securities into their Accounts. Should they do so, Strategic Advisers or its designee will liquidate those securities as soon as reasonably practicable, and clients acknowledge that transferring such securities into their Accounts acts as a direction to Strategic Advisers to sell any such securities. Clients may realize a taxable gain or loss when these shares are sold, which may affect the after-tax performance/return within their Accounts, and Strategic Advisers does not consider the potential tax consequences of these sales when following a client's deemed direction to sell such securities. Strategic Advisers reserves the right not to accept otherwise eligible securities, at its sole discretion. When a client funds their account with existing investments, transition results will vary depending on the number of concentrated positions, alignment with the new portfolio, and level of embedded gains. Outcomes can range from selling none of your existing positions, to selling all your existing positions. Clients may realize taxable gains or losses if eligible securities are sold.

866043.8.0