Tax-smart investment1A comprehensive suite of strategies designed to help you reach your goals faster. |

Invest in municipal bond funds or ETFs

Depending on your tax bracket and financial situation, the investment team may look to municipal bond funds and ETFs when it comes to the bond portion of your asset allocation, drawing on the extensive analysis of our in-house research team.

These investments may help you keep more of what you earn because the municipal bonds typically generate income free from federal taxes and, in some cases, state taxes.

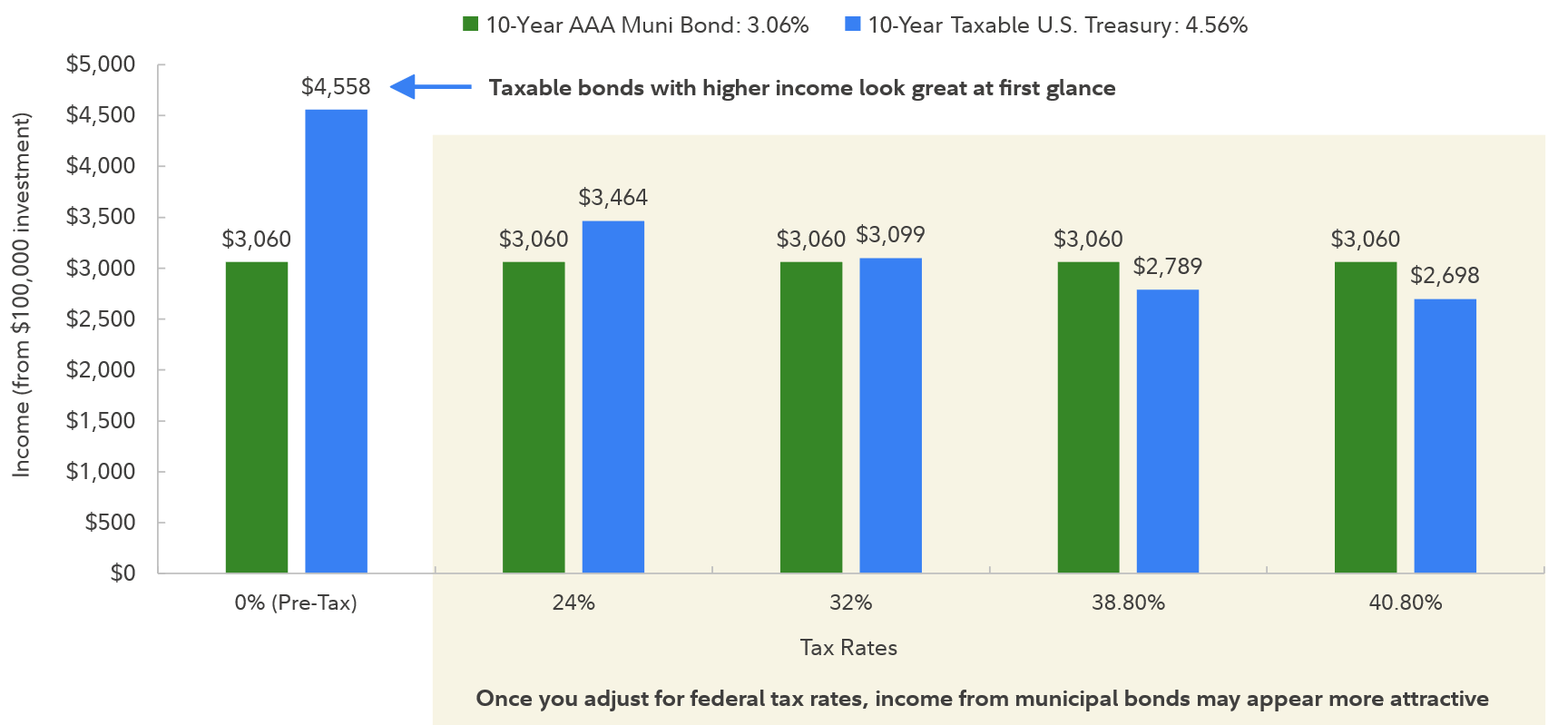

While municipal bond yields are often lower than similarly rated taxable bonds, when you adjust for federal tax rates, their after-tax yields may actually be higher.

A closer look at after-tax yields shows that income from municipal bonds may be more attractive

FOR ILLUSTRATIVE PURPOSES ONLY. This hypothetical example shows annual income from a $100,000 investment in a taxable account and the impact to that income from the four highest Federal tax rates. The municipal bond investment has a 3.06% assumed yield and the taxable US Treasury yield is assumed to be 4.56% yield (Thomson Reuters and Fidelity Investments, respectively, as of 06/30/2024). This hypothetical example is used for illustrative purposes only; actual investment results may vary. It does not reflect the impact of state taxes, federal and/or state alternative minimum taxes, tax credits, exemptions, fees, or expenses. If it did, after-tax income might be lower. Please consult a tax advisor for further details. All or a portion of the income may be subject to the federal alternative minimum tax. Income attributable to capital gains are usually subject to both state and federal income taxes. Rate includes a Medicare surtax of 3.8% imposed by the Patient Protection and Affordable Care Act of 2010.

In general, the bond market is volatile, and fixed income securities carry interest rate risk. (As interest rates rise, bond prices usually fall, and vice versa. This effect is usually more pronounced for longer-term securities.) Fixed income securities also carry inflation risk, liquidity risk, call risk, and credit and default risks for both issuers and counterparties. Unlike individual bonds, most bond funds do not have a maturity date, so holding them until maturity to avoid losses caused by price volatility is not possible.

The municipal market can be affected by adverse tax, legislative or political changes and the financial condition of the issuers of municipal funds. Although municipal funds seek to provide interest dividends exempt from federal income taxes and some of these funds may seek to generate income that is also exempt from the federal alternative minimum tax, outcomes cannot be guaranteed, and the funds may generate some income subject to these taxes. Income from these funds is usually subject to state and local income taxes.

In general, the bond market is volatile, and fixed income securities carry interest rate risk. (As interest rates rise, bond prices usually fall, and vice versa. This effect is usually more pronounced for longer-term securities.) Fixed income securities also carry inflation risk, liquidity risk, call risk, and credit and default risks for both issuers and counterparties. Unlike individual bonds, most bond funds do not have a maturity date, so holding them until maturity to avoid losses caused by price volatility is not possible.

The municipal market can be affected by adverse tax, legislative or political changes and the financial condition of the issuers of municipal funds. Although municipal funds seek to provide interest dividends exempt from federal income taxes and some of these funds may seek to generate income that is also exempt from the federal alternative minimum tax, outcomes cannot be guaranteed, and the funds may generate some income subject to these taxes. Income from these funds is usually subject to state and local income taxes.

1. Tax-smart (i.e., tax-sensitive) investing techniques (including tax-loss harvesting) are applied in managing certain taxable accounts on a limited basis, at the discretion of the portfolio manager primarily with respect to determining when assets in a client's account should be bought or sold. As the discretionary portfolio manager, Strategic Advisers LLC ("Strategic Advisers") may elect to sell assets in an account at any time. A client may have a gain or loss when assets are sold. There are no guarantees as to the effectiveness of the tax-smart investing techniques applied in serving to reduce or minimize a client's overall tax liabilities, or as to the tax results that may be generated by a given transaction. Strategic Advisers does not currently invest in tax-deferred products, such as variable insurance products, or in tax-managed funds, but may do so in the future if it deems such to be appropriate for a client. Strategic Advisers does not actively manage for alternative minimum taxes; state or local taxes; foreign taxes on non-U.S. investments; federal tax rules applicable to entities; or estate, gift, or generation-skipping transfer taxes. Strategic Advisers relies on information provided by clients in an effort to provide tax-sensitive investment management and does not offer tax advice. Except where Fidelity Personal Trust Company (FPTC) is serving as trustee, clients are responsible for all tax liabilities arising from transactions in their accounts, for the adequacy and accuracy of any positions taken on tax returns, for the actual filing of tax returns, and for the remittance of tax payments to taxing authorities.

866043.8.0